Can I Afford Shared Ownership?

What Will I Pay Each Month?

We’re here to be transparent about the real costs of homeownership. With Shared Ownership, your monthly payments are made up of several parts:

- Mortgage repayments (on the share you own)

- Rent (on the share you don’t own)

- Service charge

- Council tax and utilities (variable)

And one-time costs like solicitor fees, reservation fees, deposit. Everyone’s financial situation is unique - and our goal is to ensure the home you love is affordable and sustainable for you. That’s why every applicant for Shared Ownership must go through a personal affordability assessment before we can offer a home.As part of this process, we’ll provide you with a Key Information Document (KID). This gives you a clear, personalised breakdown of the costs involved, including your estimated monthly payments and upfront expenses so you know exactly what to expect before you commit.

Affordability Assessment: What to Expect and What You’ll Need

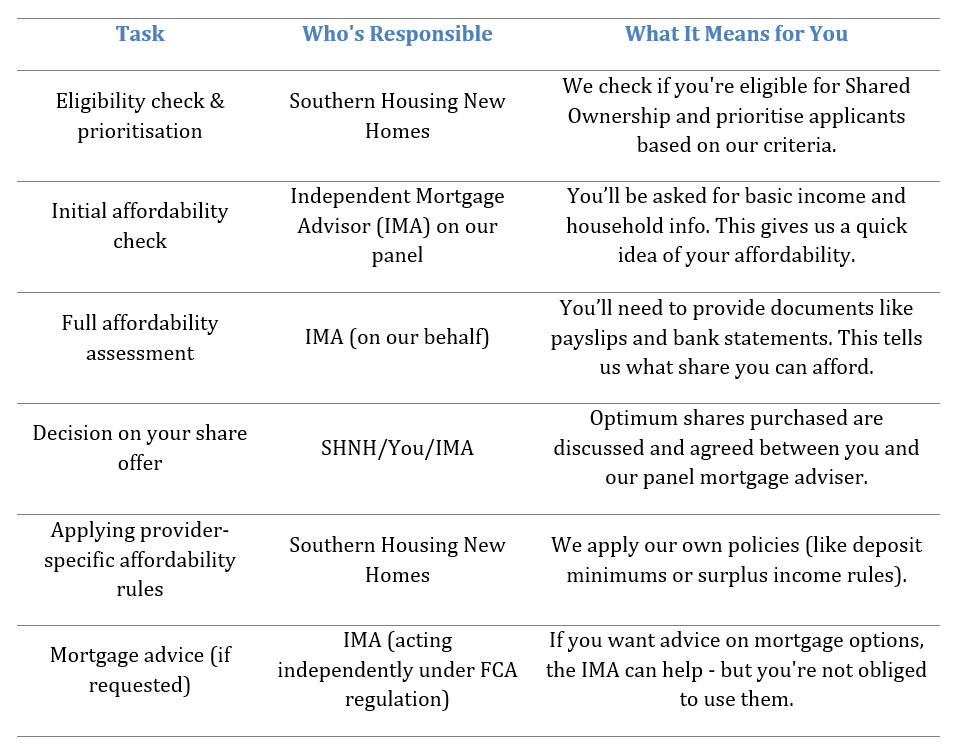

Before you can reserve a home with Southern Housing New Homes, we’ll need to make sure the property is genuinely affordable for you. This is a requirement for everyone applying to buy a Shared Ownership home, and it's an important step in ensuring the initiative is the right fit for your circumstances.

🔍 What is an affordability assessment?

This is a financial review carried out by a specialist Independent Mortgage Advisor (IMA) to determine whether the home you're interested in is suitable based on your income, outgoings and deposit.Note: This is not mortgage advice and does not guarantee you will be able to get a mortgage. It is simply a step required by Homes England and us as your provider to ensure responsible and fair homeownership.It helps us and you understand whether Shared Ownership is suitable - and whether you can afford the share and monthly costs of the home you're interested in. This assessment is done independently, and you’re under no obligation to use the same advisor for your mortgage or any other financial service if you proceed.

📘 What does the assessment involve?

We operate a two-stage affordability process:

Stage 1 - Initial Assessment

- Independent Mortgage advisor will carry out a basic free initial check to confirm your eligibility and readiness to proceed. You’ll asked about your basic income and household info.

Stage 2 – Full financial review

- The panel Independent Mortgage Advisor (IMA) will carry out a more detailed assessment, including a review of your income, monthly costs, and deposit

- This stage confirms the maximum share you can purchase and ensures long-term affordability

Who carries out the assessment?

Southern Housing New Homes works with a panel of trusted Independent Mortgage Advisors (IMAs) who are experienced in Shared Ownership and regulated by the Financial Conduct Authority (FCA). You’ll be referred to one of these IMAs before your viewing or when you're ready to proceed.

You are also free to use your own mortgage advisor if you prefer - but they must be qualified and experienced in Shared Ownership.

💡 Why use a panel IMA?

Panel advisors are already familiar with our processes and developments. They can offer clear guidance, quicker turnarounds, and ensure your assessment meets the Capital Funding Guide standards.

📑 What documents will I need to provide?

You’ll need to upload a set of supporting documents when submitting your application. This helps the IMA complete your assessment quickly.

Required documents include:

- Proof of ID (passport or driving licence)

- Last 3 months of payslips (or proof of income if self-employed)

- Last 3 months of bank statements

- Proof of deposit or savings

- Credit commitments (e.g. loans, credit card balances)

What’s included in the affordability check?

Your IMA will look at:

- Your household income and employment

- Monthly outgoings, including debts and dependants

- Savings available for your deposit

- Estimated monthly housing costs (rent, mortgage, service charge)

- Affordability against Homes England and SHNH policy criteria

- They will also advise on the share size you can afford and, if applicable, highlight any barriers that may need resolving.

👇 Good to Know:

- You are free to choose any mortgage advisor. We recommend our panel advisors because they know the process and can move things quicker.

- The initial affordability check is free, and you’re not tied to that advisor later unless you want to continue with them.

- You can find our affordability criteria and FAQs on our Shared Ownership page and in your account dashboard.

🛡️ Our policies and what they mean for you

As part of our commitment to fairness and transparency, we follow a number of key policies when assessing applications:

- Minimum Surplus Income Policy – you must have a set amount of income left over each month after all bills and housing costs

- Minimum Deposit Policy – you must have a minimum deposit (usually 5–10%) depending on lender requirements

- Adverse Credit Consideration – we may not be able to proceed if you have recent credit issues; your IMA will advise

These policies are designed to protect you from unaffordable homeownership and ensure the home you choose suits your finances.

❗ What happens if you're not eligible or affordable?

We're here to help you every step of the way - but there are a few situations where we may not be able to progress your application for Shared Ownership.

Your application may be declined if:

- You don’t meet the Shared Ownership eligibility rules

- You’re unable to afford the home based on our financial assessment

- You can’t meet one or more of our policies (such as minimum income, deposit levels or other requirements)

- You’re unable or unwilling to provide the required information or documentation

- You ask to purchase a different share than what the financial assessment deems affordable, and no clear or reasonable justification is provided

If any of these apply, we’ll let you know clearly and guide you on your next steps. This could include:

- Looking at alternative homes or tenures

- Reapplying at a later stage if your circumstances change

- Getting financial advice to help plan your next move

We know that not every journey is linear - so we’ll always do our best to offer honest feedback and support wherever we can.

🧾 Who does what? Understanding the roles

What Happens Next?

If your application is successful and you’ve passed the affordability assessment:

- You’ll receive a formal offer

- You’ll be guided through reservation, legal processes, and mortgage steps

We’ll be with you at every milestone, and you can read more about The Buying Process and what to Expect when buying a New Build Home.

What to Expect During Your Journey

- Honest conversations with our Sales Team about eligibility

- Step-by-step support with paperwork and the application

- Dedicated contacts to help you progress smoothly

Frequently Asked Questions

What happens if I want to staircase?

Can I decorate or renovate my home?

What if I want to sell later?

What’s included in the service charge?

Questions or Concerns?

We’re here to help. If you have questions at any stage, or if something isn’t clear:

📞 Call us on 0300 555 2171

📩 Email us at sales@shnewhomes.co.uk

You can also read more in our Jargon Buster or check our Buying Guides.

Ready to Apply?

Explore our homes and find the right one for you. If Shared Ownership sounds like a perfect fit, start your home buying journey with Southern Housing New Homes today.